Commodity[1] and gold funds have been the big winners so far this year, with year-to-date gains of 24.6% and 5.8% respectively. Driven by inflation rates not seen in forty years and the war in Ukraine, these classic inflation “hedges” have provided investors with low correlated, positive returns during a period that’s been bad for both stocks (down 3.1%) and bonds (down 6.3%)

Chart 1: YTD performance – Gold, Commodities, Stocks and Bonds

Despite the recent outperformance of commodity and gold funds, I’ve long argued that commodity and direct gold exposure does not belong in investment portfolios because they fail a simple test of what an investment is. An investment, for portfolio purposes, is a security with a positive expected cash flow associated with it such that the holder (investor), need not do anything other than collect cash flows in order to expect a positive return on their investment. If they also ultimately sell the security for more than they paid for it (capital gain) that is icing on the cake.

For stocks, these cash flows are dividends and share buybacks and for bonds these are periodic interest payments. In contrast, exposure to commodities and gold offer no expected cash flow to the holder. The only way to make money on commodity and gold exposure is to sell what you hold to someone else for more than you paid. A strategy better described as “speculation”.

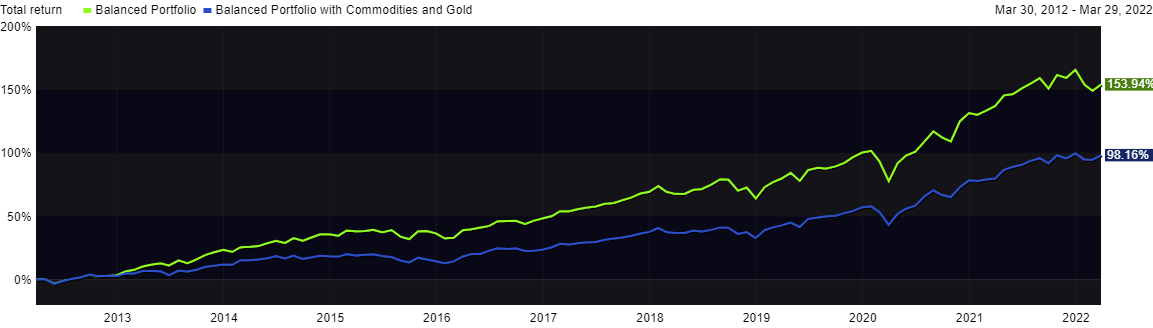

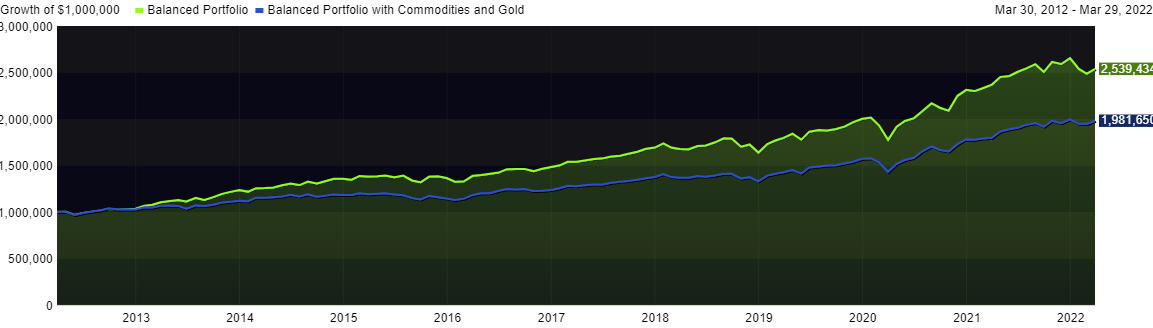

We can more fully understand the impact of a long-term strategic allocation to commodities and gold by comparing a standard balanced portfolio to a balanced portfolio with 10% allocations to commodities and gold.

Chart 2: 10-Year Total Return of Balanced vs Balanced with Commodities and Gold

Chart 3: 10-Year Impact on $1 million Invested: Balanced vs Balanced with Commodities and Gold

We can see that long-term allocations to non-cash flow assets such as commodities and gold created a significant drag on portfolio performance (even including recent outperformance). In this example, the cost of owning commodities and gold on a $1 million portfolio was almost $600,000 over ten years.

When selecting the building blocks of an investment portfolio, it is critical to consider the source of expected return. Traditional asset classes such as stocks and bonds have positive expected returns primarily due to their expected future cash flows. Ignoring this aspect of potential investments can prove costly over time.

[1] As of 3/29/22 Bloomberg Commodity Index, spot Gold, Russell 3000 (U.S. stocks), Barclays Aggregate (U.S. bonds).