With the potential debt limit crisis behind us now (for two years anyway), this is a good time for investors to take a step back and see how they reacted to the possibility of a market meltdown. At our firm, we spend a considerable amount of time stress testing portfolio asset allocations with clients. Stress testing entails running the current portfolio through some type of really bad market environment to get a sense of what the experience would be like for the client if they held that portfolio during a turbulent market. The result of this process is, hopefully, a portfolio asset allocation that reasonably reflects the client’s comfort with downside risk and the tradeoff that exists for all investors. (i.e., safer portfolio = less volatility, less upside: more aggressive portfolio = more volatility, more upside).

Once we have the portfolio allocation set, then all clients need to do when markets are volatile (or potentially volatile in the case of the recent debt limit situation) is to stay in their seat and ride things out, knowing that the portfolio should behave in such a way that they can live with it (because that is explicitly how we arrived at that allocation).

With the latest crisis behind us, it’s worth exploring what an alternative reaction to a first ever U.S. default might have looked like. What else could an investor have done besides sit in their seat?

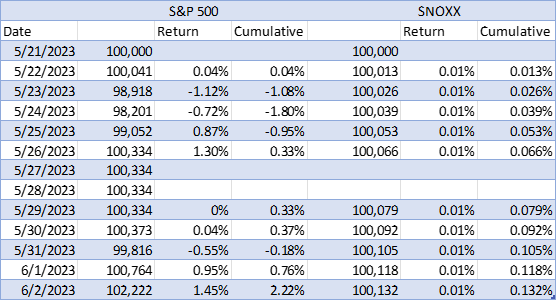

Let us imagine it’s the weekend of May 20 – May 21 and the most updated “X-date”[1] is June 5, and you’re relaxing with friends. While chatting, the subject of the potential debt default comes up. By Sunday night, your friends have convinced you to get out of the market first thing Monday morning and get back in after the dust settles. So, the morning of Monday May 22, you sell out of $100,000 of S&P 500 ETF (SPY)[2]. You take the proceeds and place them in a money market mutual fund that holds short-term Treasury bonds (Schwab Treasury Obligations Money Fund – Investor Shares – (SNOXX[3])).

Here are the daily returns for each investment over the next week.

On Saturday, June 3, President Biden signed the Fiscal Responsibility Act of 2023 which suspended the debt limit for two years and ended the potential debt limit crisis.

During the hiatus from the market, the S&P 500 outperformed the money market fund by about 2%. While this doesn’t look like much, once we annualize the return to account for the short investment period, we can see how damaging market timing turned out to be. On an annualized basis, the S&P 500 outperformed the money market by about 90%.

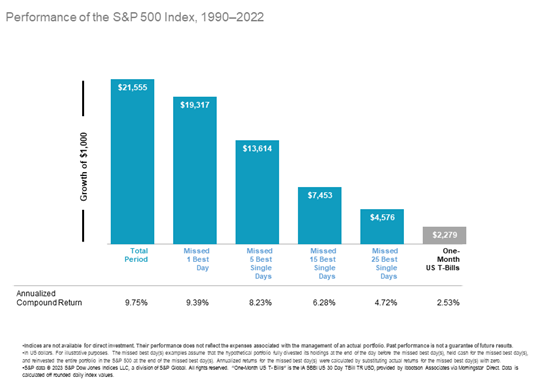

While one can quibble about the exit and re-entry dates and that would certainly have had an impact on the results, this hypothetical is consistent with research that shows how difficult it is to “win” at market timing. The chart below shows the performance of the S&P 500 over the period 1990-2022 (9.75% annualized) and compares that return to the returns earned by market timers that miss just a handful of the best trading days over the 33-year period. Missing just the 25 best trading days over 33 years reduced the realized return by over 50%. What this demonstrates is just how precise one needs to be in order to outperform the market through timing.

As we move on from the debt limit crisis (does anyone even remember this anymore?), one thing to keep in mind is that market timing is market timing no matter what the rationale is. And we know that the likelihood of “winning” at market timing is extremely low. The best approach for investors concerned about volatility is to match their portfolio asset allocation to the level of volatility they can live with so there won’t be a need to “sell now and buy back when the danger passes”. Ultimately, investors are better off accepting that there is always potential for market volatility and the best way to manage it is through planning and a willingness to stay in their seat.

[1] The X-date refers to the date on which the U.S. government would no longer be able to meet its financial obligations

[2] For simplicity, we ignore taxes and transaction costs

[3] The daily returns are simulated based on the current SNOXX yield of about 4.8%