Since the beginning of 2021, inflation has increased significantly, driven largely by supply and demand changes caused by the Covid pandemic. Last week, the Labor Department reported a 6.8% year over year increase in the Consumer Price Index, the highest in thirty-nine years. Investors are justifiably concerned about the potential impact of inflation on portfolio performance. And, not entirely surprising, there is no shortage of recommendations from Wall Street and the financial press on how investors can protect their portfolios from the ravages of inflation. A recent Wall Street Journal article offered a grab bag of inflation fighting products for investors to pick from.

Legitimate cause for concern?

It is worth taking a moment to consider why inflation might, in fact, be bad for stocks and bonds. Following are some potential causes for poor stock and bond returns due to higher inflation.

Why inflation could be bad for equities

- Cost of inputs – an increase in the cost of inputs (materials and/or labor) for companies that cannot pass along costs, would cause profit margins to decline and could lead to a decline in stock prices to reflect reduced profitability.

- An increase in interest rates in response to inflation – would lead to

- Increase in borrowing costs, reducing profitability

- Increase in the discount rates used to value future cash flows, reducing the value of future cash flows.

- Higher yielding fixed income as rates rise would compete for investor dollars reducing demand for stocks.

Why inflation could be bad for fixed income

- Fixed nature of standard bond payments – higher inflation would reduce the value of the fixed payments.

- An increase in interest rates in response to inflation – would lead to Interim (prior to maturity) capital losses. Bond prices decline when interest rates rise so that the yield (coupon divided by bond price) stays in line with current market yields.

So, there is cause for rational concern about the potential impact of higher inflation on the basic portfolio building blocks. But before we jump in headfirst to inflation protection mode, let’s take a look at how a basic portfolio has actually performed during periods of high inflation.

Generic Portfolio Performance in an Inflationary Environment

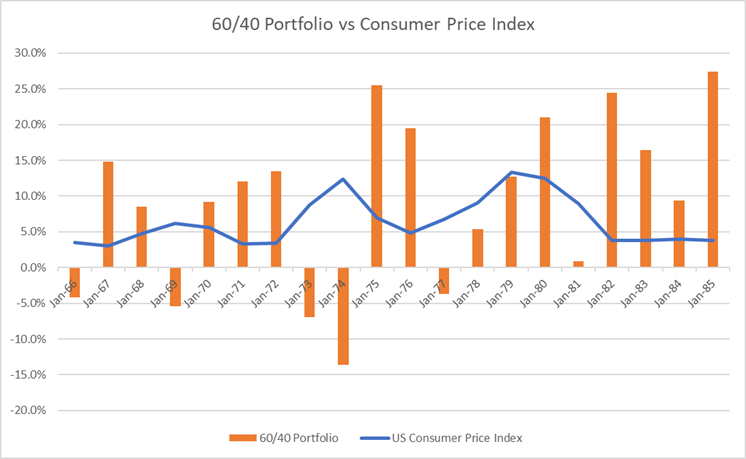

We can take a high-level look at this by examining how a standard 60% equity/40% fixed income portfolio[1] performed during a past inflationary period.

In the twenty-year period beginning January 1966 through December 1985, the US CPI exceeded 3% every year and averaged 6.4% per year.

Following are summary data points for the hypothetical portfolio performance:

- The portfolio generated a positive nominal return in 15 out of 20 years (75%)

- The portfolio generated a positive real return (adjusted for inflation) in 12 out of 20 years (60%)

- Over the full period, the 60/40 portfolio returned an annualized 8.7% vs 6.4% inflation

- Correlation[2] of returns over the twenty-year period was -0.004 suggesting that there was no clear relationship between inflation and portfolio returns.

So does this mean inflation does not matter. No, but it does suggest that as with most things related to investing, reality is significantly more complicated than a headline might suggest. Many factors impact the performance of individual asset classes and diversified portfolios, inflation being just one of them. Focusing on the risks of inflation alone overly simplifies the challenges of predicting investment returns.

The key takeaway for investors is to ensure not to overreact to headlines, whether they be about inflation spikes or other potentially vexing financial trends.

[1] 60% S&P 500 index and 40% five-year treasury notes rebalanced annually

[2] Correlation is measured between 1 (asset returns move perfectly together) and -1 (asset returns move in perfectly opposite direction). A correlation of zero suggests no relationship between the asset returns.