“Stocks are expensive, what should we do?“

With stock markets continuing to make all-time highs on a regular basis following a 112.6%[1] gain off the March 23, 2020, COVID-19 lows, there’s a fair amount of “stocks are expensive, what should we do” discussion.

The implicit concern expressed here is that if markets are expensive, there is a higher likelihood of a market meltdown. The reality, however, is that stocks are always risky and cheaper markets don’t necessarily protect investors against the risk of a market collapse. Cheap stocks can always get cheaper.

A more constructive way to think about high market valuations is to consider a simple, mathematical equivalent to valuation: expected future return.

The Price/Earnings (P/E) Ratio

The most common approach to stock valuation is a measure called the price to earnings multiple (P/E) which looks at how much an investor is paying for a certain amount of corporate earnings. For example, pay $10 for a share of stock of a company that generates $1 of earnings per share, and the P/E multiple you paid is ten. Pay $30 for the same share of stock and the P/E multiple you paid is 30. The same concept can be applied to the overall stock market to give a sense of how cheap or expensive the market is.

The Earnings Yield (E/P)

We can think more constructively about valuations by flipping the P/E ratio over to give us E/P, a measure called the ‘earnings yield’. This measure says for every “P” dollars invested, how much in earnings should I expect to receive in the future. Using the examples above, a P/E of 10 becomes an earnings yield of 10% while a P/E of 30 becomes an earnings yield of about 3%.

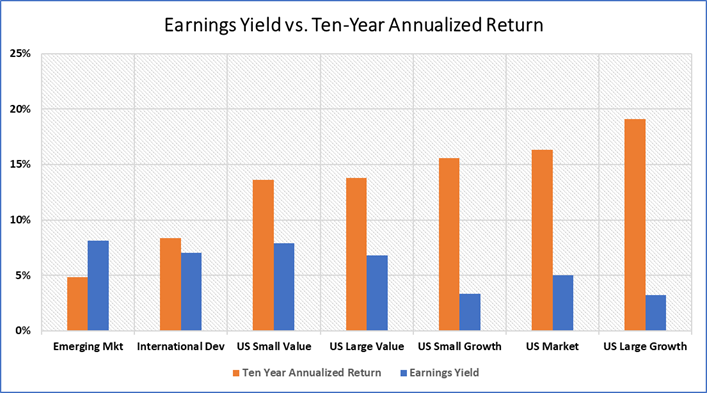

We can use the earnings yield as a simple approach to setting realistic expectations around future stock returns. The chart below compares current earnings yields on a variety of market segments to their previous ten-year annualized returns. What the data show is that “expensive” is just another way of saying “lower future expected returns”.

Chart 1: Earnings Yield vs. Ten-Year Annual Realized Returns

Source: Kwanti – Ten year annualized returns as of 11/2/21 and Vanguard – P/E ratios as of 9/30/21

To answer the initially posed question, “stocks are expensive, what should we do? “, investors can reframe the question in a more constructive way by viewing expensive stocks as stocks having a lower future expected return. So, the question becomes “stocks have a lower expected return, what should we do”. The answer is to accept what the market is offering and set realistic expectations for future returns. This approach has the benefit of reducing worries about market corrections and enables financial planning based on reasonable expectations.

[1] The Russell 3000 index return from March 23, 2020 through November 2, 2021