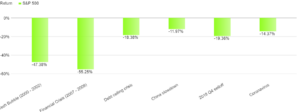

From February 20th, 2020 through March 23rd, 2020, the S&P 500 plummeted 34%. Concerns about the human and economic impact of the Coronavirus drove stock prices to down at a historic pace. Since then, in the U.S., we have seen tens of thousands lose their lives, millions of jobs lost and business activity ground to a standstill with little clarity as to when life will return to something approaching normal. And yet, over the same period, the S&P 500 is up almost 30%. In fact, since the beginning of the downturn in the market, the cumulative loss on the S&P 500 is only 14%. To put this in perspective, the chart below compares the performance of the S&P 500 during the Coronavirus pandemic to other market disruptions. It does make one wonder why the market is not lower than it is.

Chart 1: S&P 500 Total Return During Various Crises

Note: Coronavirus dates 2/20/20 – 04/27/20

Possible explanations for why the market is not down more include that the market is just wrong, or this is a ‘fake’ market. But, in reality, the market is a massive information discounting machine. The results of the market discounting process are neither right nor wrong (and certainly not fake). It is the weighted expectation of all market participants based on available information. So, what available information suggests that the market should not be much lower than it is given what we see in the economy?

A simple model of market returns can help us understand how the market could be where it is. The Gordon Growth Model is a model that looks at a stock (or market) price as a function of three variables. It assumes the three variables are stable in perpetuity.

P = E/R-g, where…

P = Stock (or market) price, E = Earnings, R = Equity Cost of Capital (equity premium plus the risk-free rate), g = Long Run Growth Rate

The key to understanding why the market does not necessarily need to be lower than it is, is separating the short run from the long run. In the short run, the pandemic’s impact on growth and earnings is massive. However, the value of stocks derives largely from the perpetual nature of equity cash flows. Suppose we skip ahead one year and estimate values for the Gordon Growth Model beginning at the end of 2020. Can we develop estimates that result in market prices consistent with what we see today?

Table 1: S&P 500 Estimated Price based on Gordon Growth Model

Source: 2019 earnings estimate, IBES; S&P 500 prices as of 12/31/2019 and 4/28/2020, Risk free rate is the yield on the ten-year treasury bond.

The table includes a set of estimates that brings us to an S&P 500 market price we see today. This analysis by no means suggests the current market price is “right”. Rather, it is an opportunity to understand why the market might not be lower than it is by focusing on the levers that drive market prices. The key takeaways are that market prices are primarily driven by the perpetual nature of equity cash flows, interest rates and the equity risk premium. In the example above, the decline in interest rates and the perpetual cash flows largely offset the decline in earnings and the increase in the equity risk premium, resulting in a market price down roughly 11% from the beginning of 2020.