On February 19th, 2020, the S&P 500 index closed at 3,386.15. That marked the highpoint before the COVID-19 pandemic and subsequent global economic collapse drove the U.S. stock market down 33% in a little over a month. On August 18th, 2020, amid the continuing twin global disasters, the S&P 500 set a new record high. Below are five key takeaways for investors drawn from this market experience.

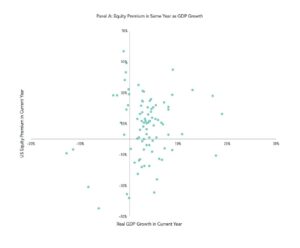

- The economy and the stock market are not the same. This has always been true, but the COVID-19 pandemic and its impact has made this lack of relationship more apparent than ever. As reviewed in a previous blog post, research from Dimensional Fund Advisors has shown there is essentially no relationship between contemporaneous Gross Domestic Product (GDP) growth and stock market performance. The key takeaway for investors is that attempting to predict market performance based on economic indicators is a fruitless exercise.

Chart 1: US equity premium vs. GDP growth, 1930—2019

Source: Dimensional Fund Advisors

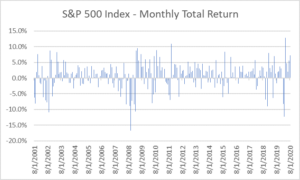

- Markets are unpredictable. At the end of August 2019, would any pundit have predicted that a global pandemic and ensuing economic collapse was around the corner? Exceedingly unlikely. Taking it one step further, assuming they called the pandemic correctly, how likely is it they would peg the 2020 market return correctly (i.e. given all the terrible news, the U.S. stock market will post a positive return through August 2020). The key takeaway for investors is that unless you think you found the next Nostradamus, act on pundit predictions at your own risk.

Chart 2: S&P 500 Monthly Total Returns – August 2001 – August 2020

Source: Dimensional – Returns Web

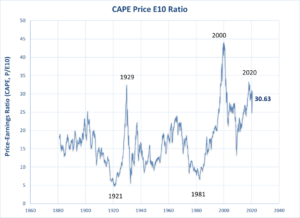

- Valuations are at historical highs. A 53% gain for the S&P 500 since the March 23rd, 2020 COVID-19-driven market-bottom combined with profit declines across much of the economy has driven market valuations to record highs. According to Professor Robert Shiller’s CAPE 10, a well know valuation model, the S&P 500 is trading at 30 times trailing ten year adjusted earnings. The market has exceeded this valuation level only twice since 1881, in 1929 and 2000. Does this suggest a market crash similar to those that followed the 1929 and 2000 market peaks is inevitable? There is no way to say with any confidence. What we do know, however, is that higher valuations are mathematically equivalent to lower future expected returns. How those lower returns are realized is unknown, but it is helpful to set realistic expectations regarding future stock returns. The key takeaway for investors is that based on current high stock valuations, modest future stock returns is a reasonable expectation.

Chart 3: Shiller CAPE 10 Ratio – 1871 – 2020

Source: Robert Shiller (http://www.econ.yale.edu/~shiller/data.htm)

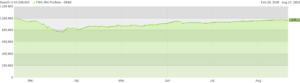

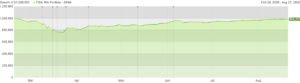

- Rebalancing Works. Portfolio rebalancing is disciplined periodic or contingent trading designed to move portfolios back to their long-term targets. Simple but not easy is a great way of thinking about rebalancing. It is in the most difficult times to stay disciplined that rebalancing pays off. The chart below shows the returns of a hypothetical 60% equity/ 40% fixed income portfolio purchased at the pre-COVID market top. The analysis looks at the portfolio performance two ways, one in which the target positions were bought and held through August 28th and another which used a contingent rebalancing algorithm[1]. Amid massive market volatility in March and April, disciplined rebalancing of portfolios paid off. One million dollars invested in the hypothetical rebalanced portfolio was, by the end of August, worth $13,000 more than the buy and hold portfolio.

Chart 4: 60/40 Portfolio – Buy and Hold vs. Rebalanced[2]

Source: Kwanti

- Stick to the plan. Your investment plan should reflect your circumstances and preferences. It should not change due to market conditions. Whether stocks are at highs, lows or anywhere in between, stick to your investment plan. The key takeaway for investors is, if you do not have a plan, get one. If you have one, stick to it. The investment plan will keep you anchored through volatile times with benefits both financial and emotional.

[1] The portfolio was rebalanced whenever a target allocation was higher or lower than its target by 10%. (i.e. a 5% position would be rebalanced if it drifted above 5.5% or below 4.5% of the portfolio). The portfolio in the chart would have been rebalanced on the following dates: 3/9/20, 3/16/20, 3/19/20, 3/25/20, 4/9/20, 5/12/20, 6/5/20). The target allocations were as follows: DFQTX DFA US Core Equity 2 24%, DFEQX DFA Short-Term Extended Quality I 20%, DFIEX DFA International Core Equity 18%, VTIP Vanguard Short-Term Infl-Prot Secs ETF 8%, VWOB Vanguard Emerging Mkts Govt Bd ETF 6%, DFCEX DFA Emerging Markets Core Equity 6%, FLOT iShares Floating Rate Bond ETF4%, DWFIX DFA World ex US Government Fxd Inc 4%, VNQ Vanguard Real Estate ETF 3%, DFITX DFA International Real Estate Sec 3%, WIP SPDR® FTSE Intl Govt Infl-Protd Bd ETF 2%, Cash 2%

[2]The results do not represent the results of actual trading using client assets, but were achieved by means of the retroactive application of a model that was designed with the benefit of hindsight. Therefore, the returns should not be considered indicative of the skill of the adviser. The results may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets.